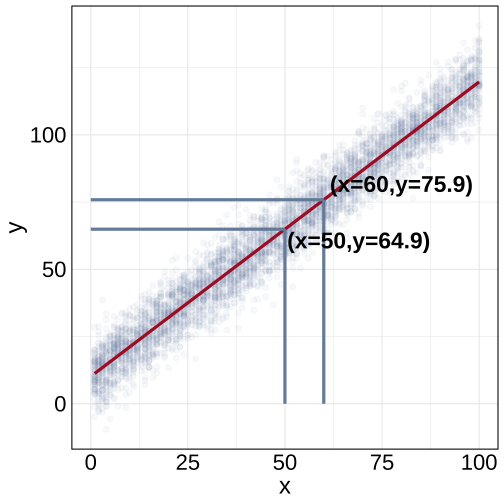

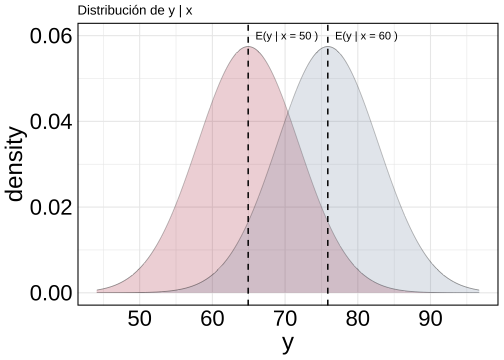

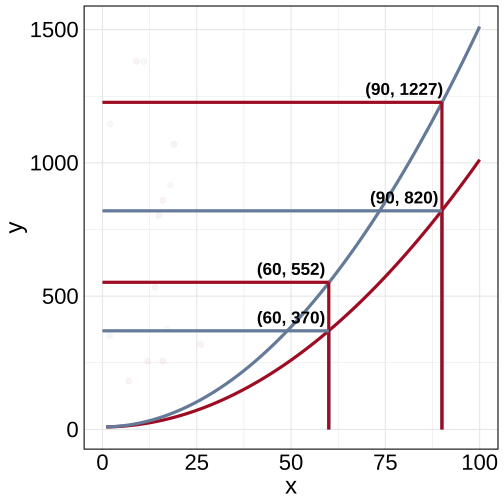

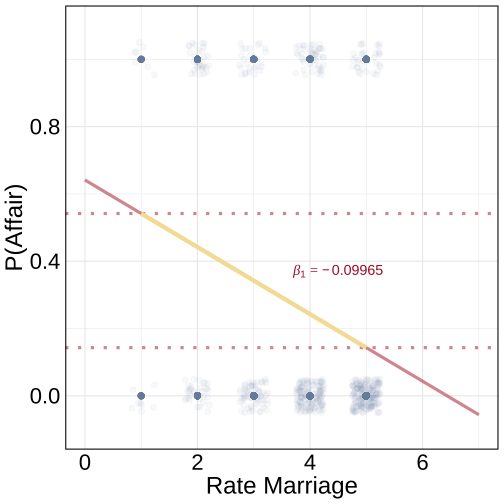

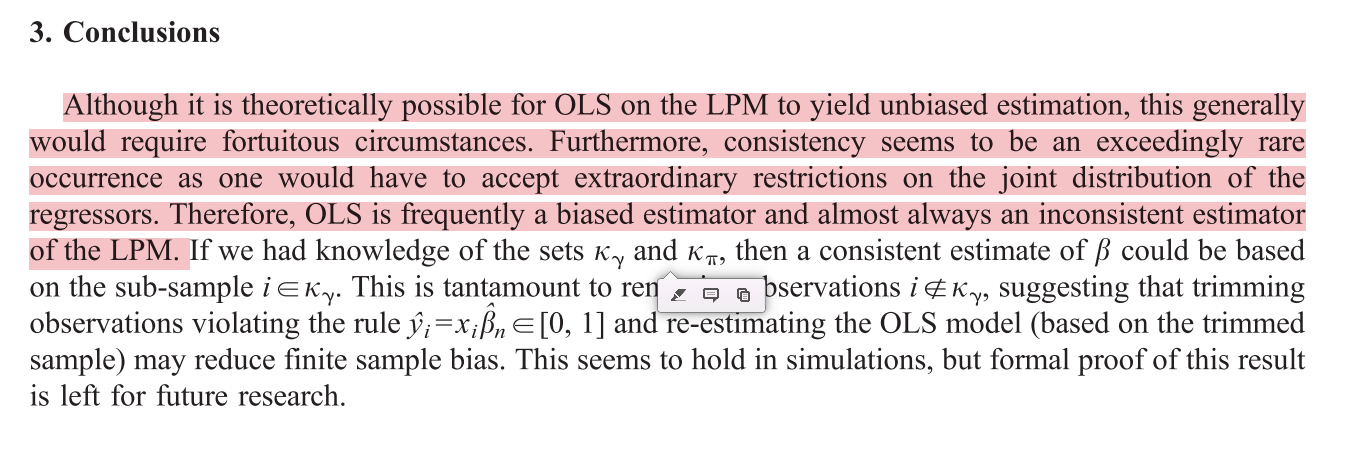

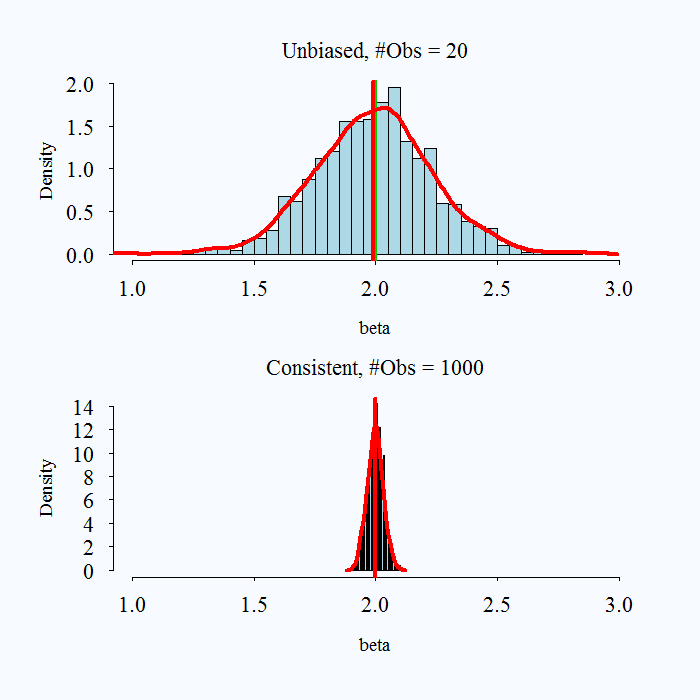

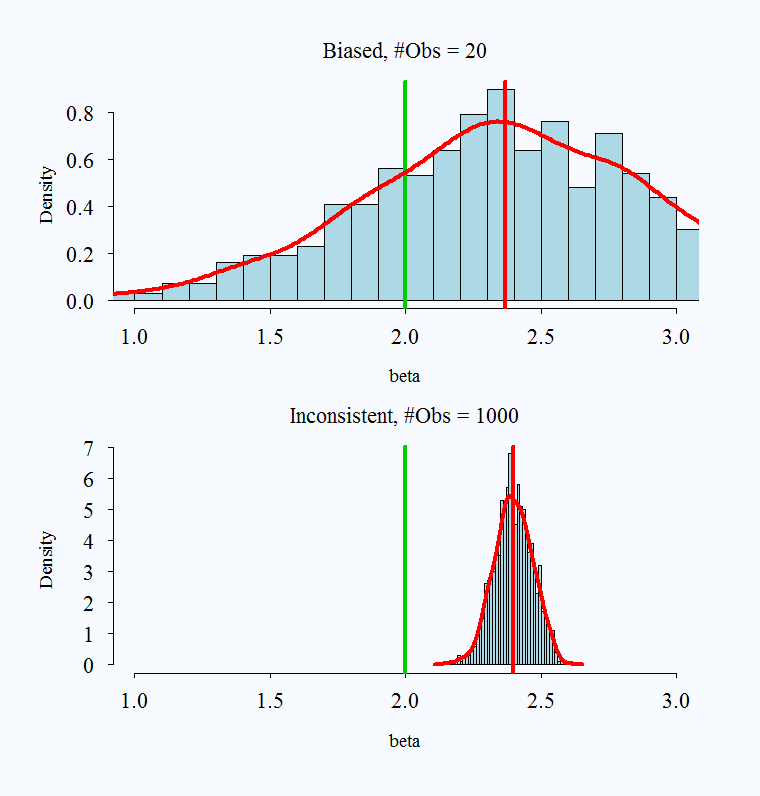

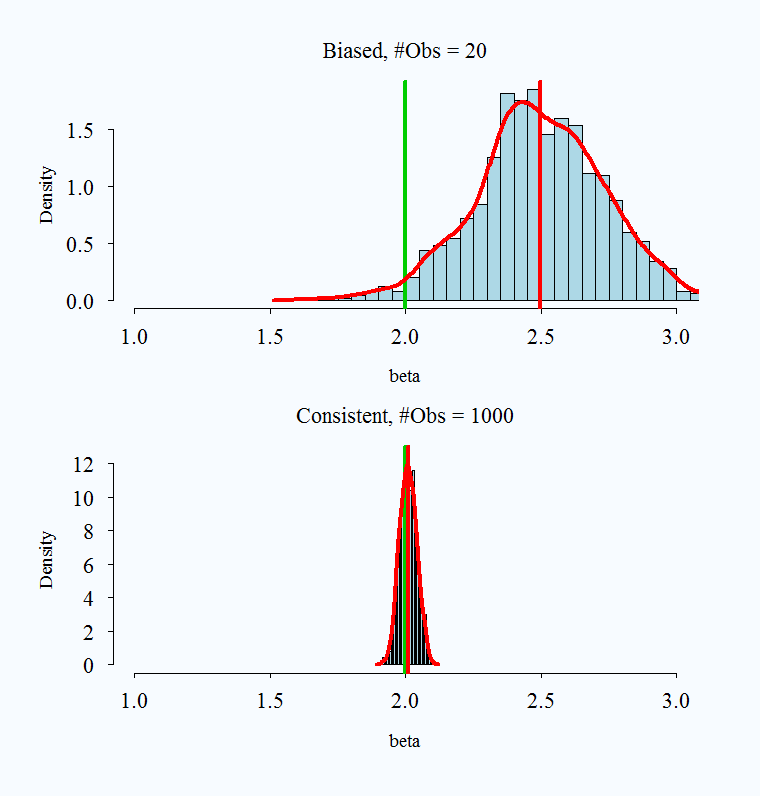

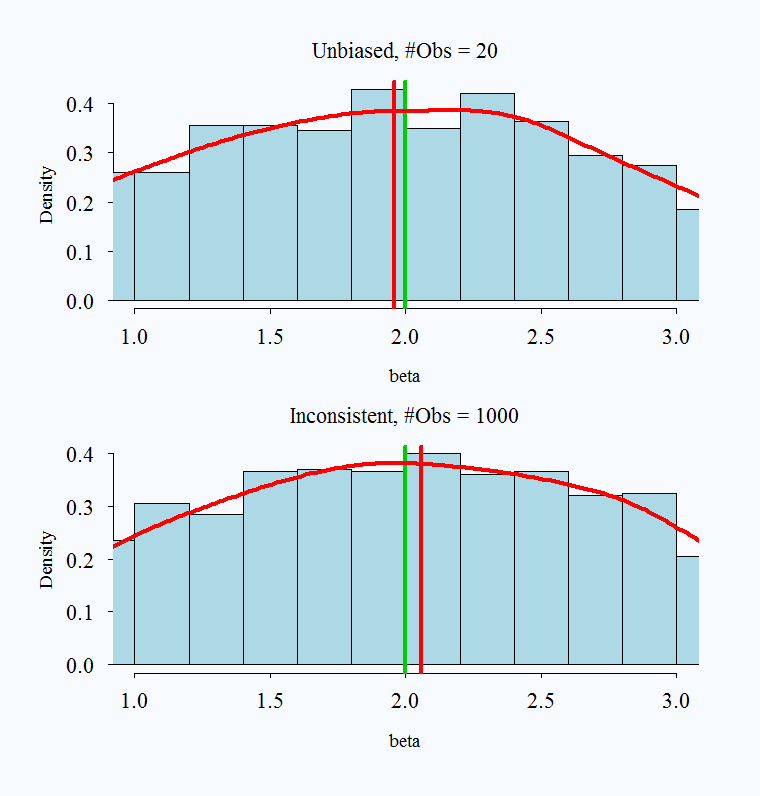

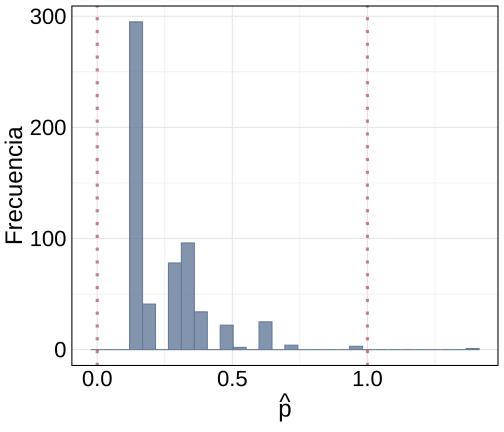

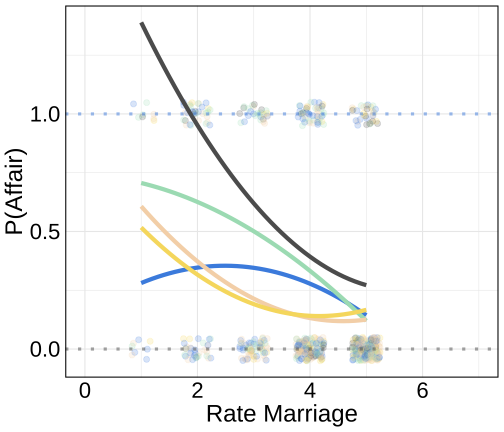

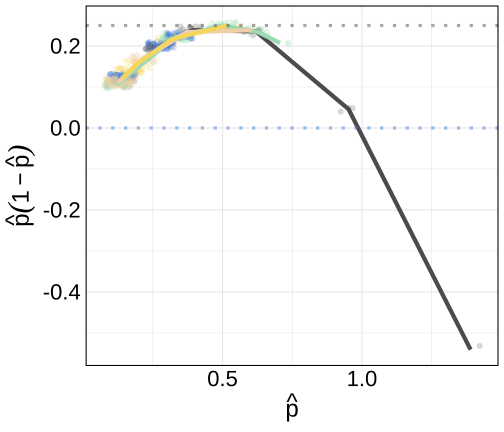

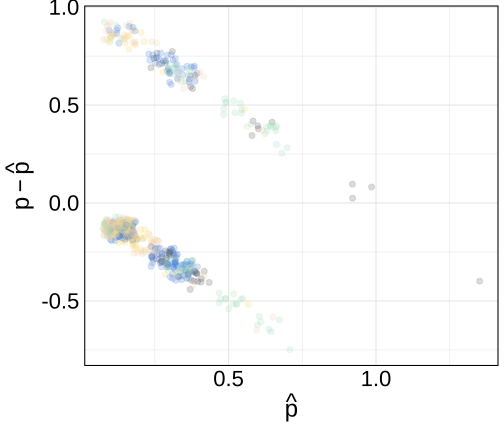

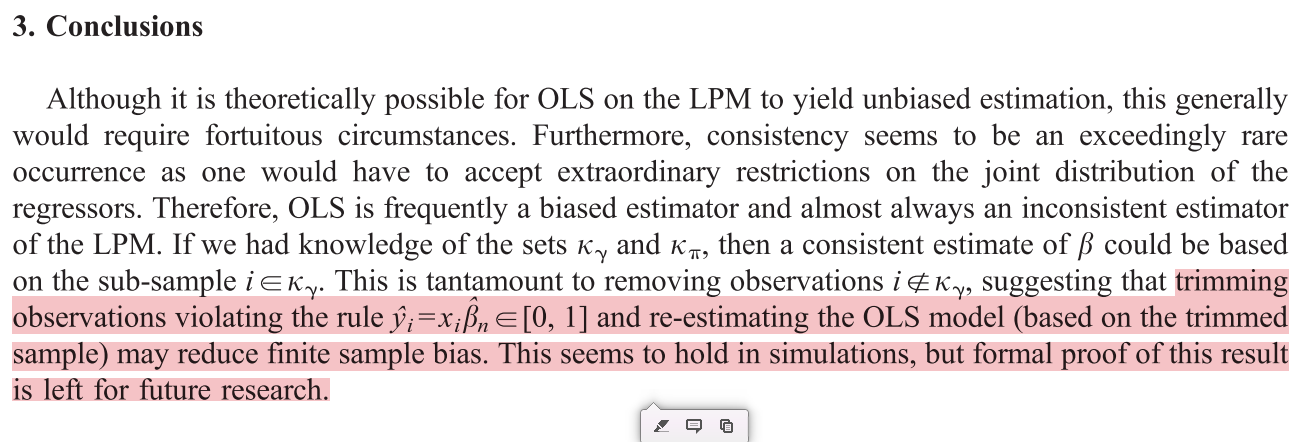

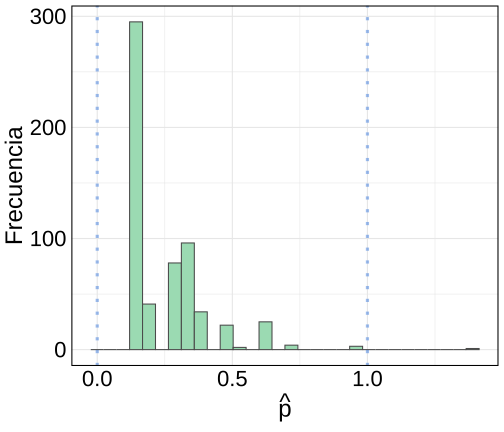

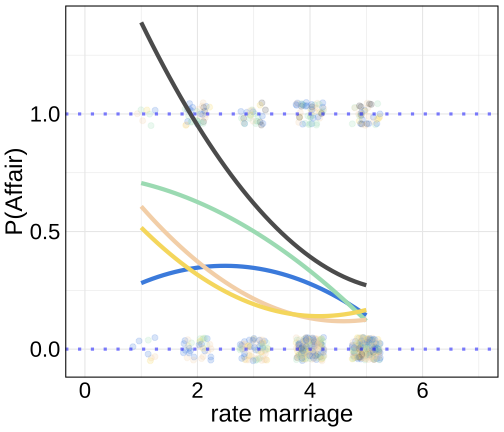

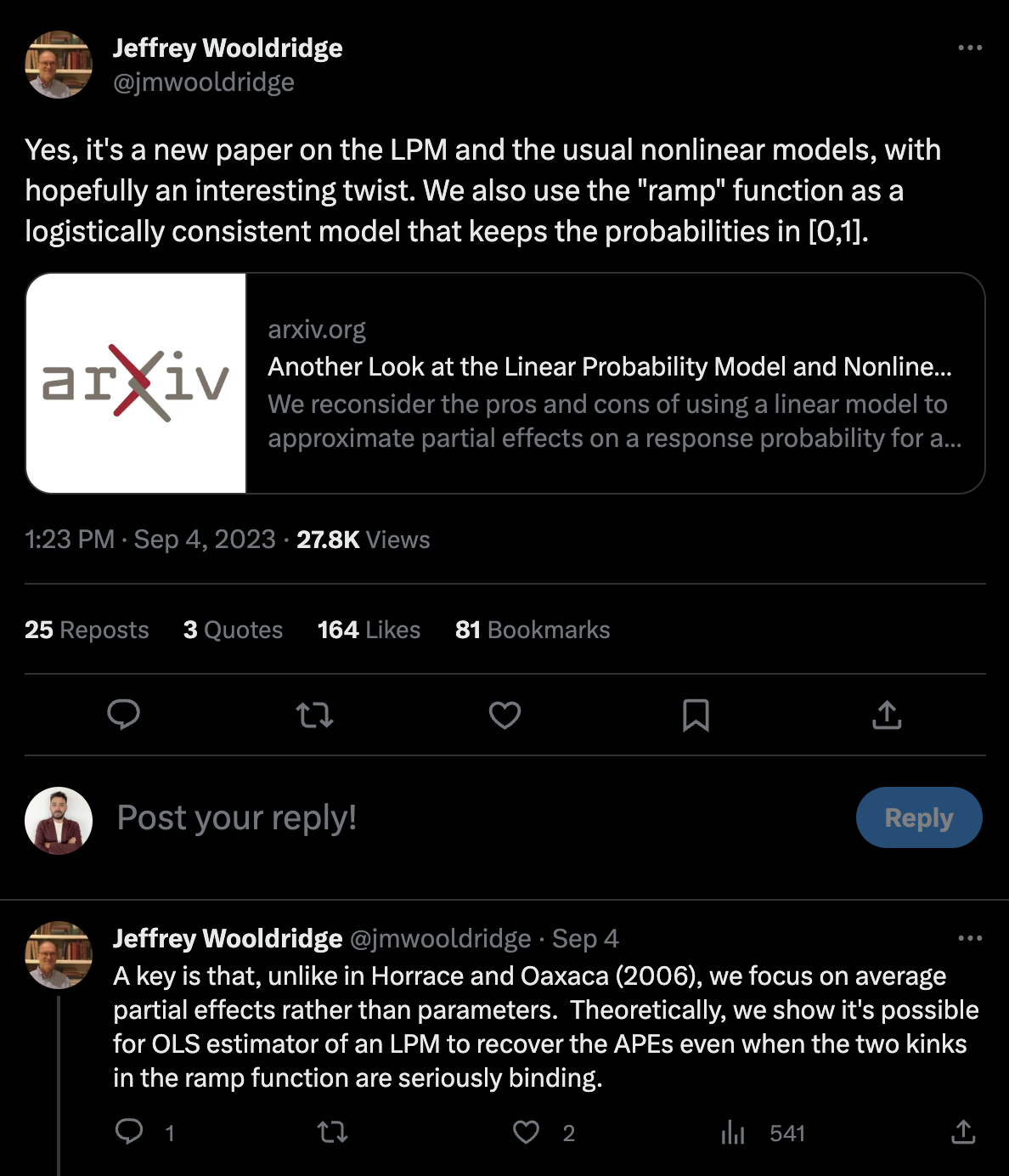

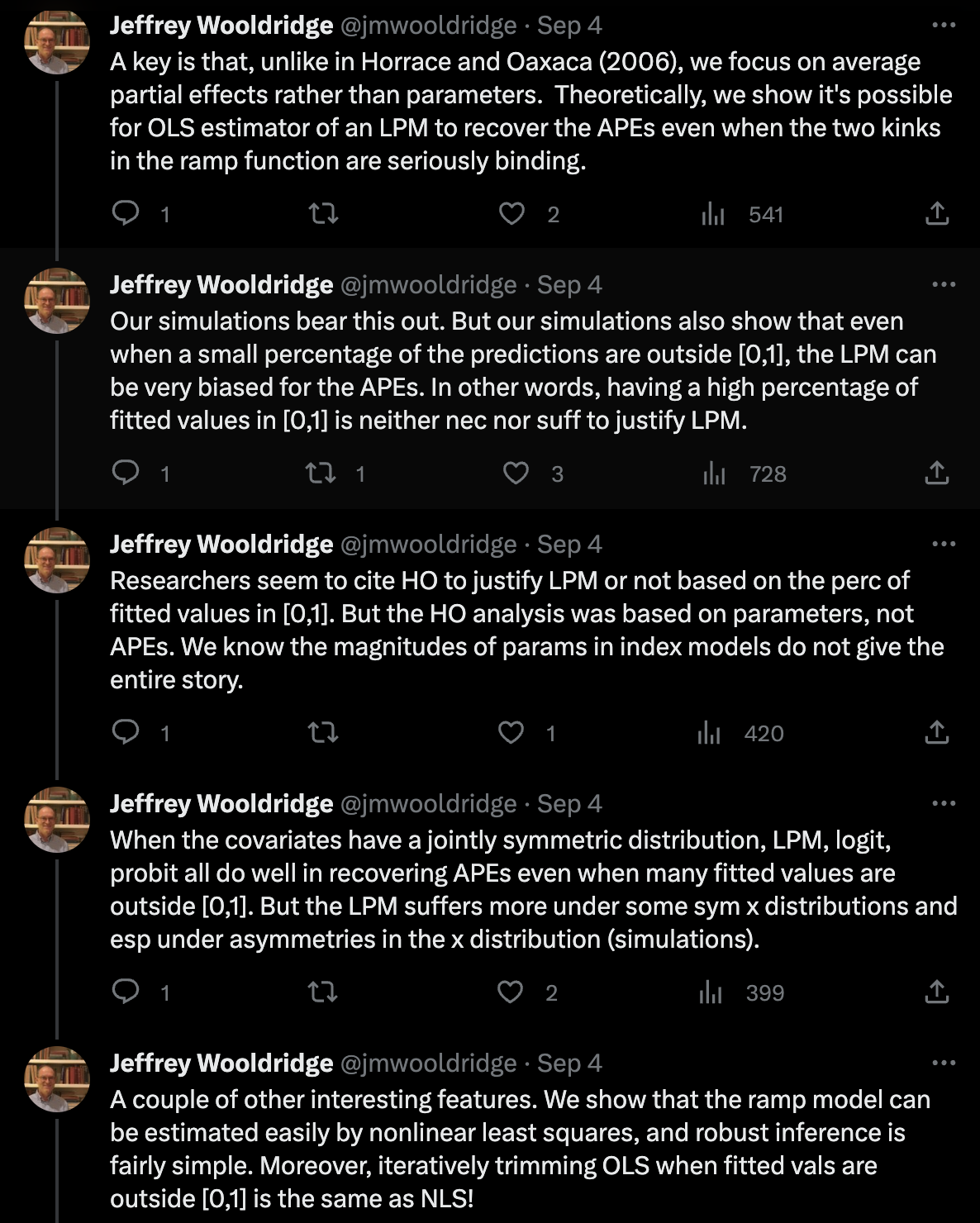

class: center, middle, inverse, title-slide .title[ # Análisis de Datos Categóricos (SOC3070) ] .subtitle[ ## Regresión Lineal y el Modelo Lineal de Probabilidad ] .author[ ### <br> Mauricio Bucca<br> Profesor Asistente, Sociología UC ] .date[ ### <a href="https://github.com/mebucca">github.com/mebucca</a> ] --- class: inverse, center, middle #Modelo Lineal de Probabilidad ##Modelos de Regresión para variable dependiente categórica --- .pull-left[  ] .pull-right[ .huge[.bold[Todo lo que siempre quisiste saber sobre regresión lineal (ˆ) ]] (ˆ) .bold[_Pero nunca te atreviste a preguntar_ ] ] --- ## Estructura de un modelo de regresión lineal Un modelo de regresión lineal estándar tiene la siguiente estructura: <br> `$$y_{i} = \overbrace{\beta_{0} + \beta_{1}x_{1i} + \dots \beta_{k}x_{ki}}^{\hat{y}} + e_{i}$$` donde: -- - `\(y\)` es la variable dependiente - `\(x_{1} \dots x_{k}\)` son predictores o variables independientes - `\(\beta_{1} \dots \beta_{k}\)` son los respectivos "efectos" de los predictores sobre `\(y\)` - `\(e\)` es un término de error aleatorio ("white noise") - `\(\hat{y} \perp e\)` --- ## Estructura de un modelo de regresión lineal Podemos repensar el LM de la siguiente forma: <br> -- .bold[Setup] - Tenemos `\(n\)` observaciones (individuos) independientes: `\(i = 1, \dots, n\)` -- - Para cada individuo observamos un valor en la variable dependiente `\(y_{i}\)`, tal que `\(y_{i} \in \mathbb{R}\)` -- - Estos resultados son realizaciones de variables aleatorias `\(\text{Normal}(\mu_{i}, \sigma_{i})\)` con media y varianza desconocida: misma distribución pero parámetros (potencialmente) distintos - Notar que es imposible identificar estos parámetros individualmente ( `\(n\)` observaciones y `\(2n\)` parámetros) --- ## Estructura de un modelo de regresión lineal El modelo de regresión lineal estándar "resuelve" este problema de la siguiente manera `$$y_{i} \sim \text{Normal}(\mu_{i}, \sigma_{i}) \quad \quad \text{ donde}$$` -- - `\(\mu_{i} = \beta_{0} + \beta_{1}x_{1i} + \dots \beta_{k}x_{ki}\)` -- `\(\quad =\mathbb{E}(y_{i} \mid x_{1}, \dots, x_{k})\)` -- - `\(\sigma^{2}_{i} = \sigma^{2}\)` -- `\(\quad =\mathbb{Var}(y_{i} \mid x_{1}, \dots, x_{k})\)` -- - `\(x_{1}, \dots, x_{k}\)` son valores fijos, no variables aleatorias -- - Todo lo anterior implica que, si `\((e_{i} = y_{i} - \mu_{i})\)`, entonces -- `\(\quad e_{i} = \text{Normal}(\mu_{i}, \sigma) - \mu_{i} \sim \text{Normal}(0, \sigma)\)` -- En resumen, .content-box-primary[ `$$\color{white}{ y_{i} \sim \text{Normal}(\mu_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = \mu_{i} + \text{Normal}(0, \sigma)}$$` ] -- Notar que LM describe los datos con `\(k + 2\)` parámetros: `\(\beta_{0}, \beta_{1}, \dots, \beta_{k}, \sigma\)` --- ## Estructura de un modelo de regresión lineal Es común encontrar el modelo lineal escrito en forma matricial: `$$\newcommand{\vect}[1]{\boldsymbol{#1}}$$` .pull-left[ `$$\vect{y} \sim \text{Normal}_{n}(\vect{X}\vect{\beta},\vect{\Sigma}) \quad \text{ donde ...}$$` ] .pull-right[ - `\(\vect{y}\)` es un vector que contiene las diferentes `\(y_{i}, \dots, y_{n}\)` - `\(\vect{\mu} = \vect{X}\vect{\beta} = \beta_{0} + \beta_{1}\vect{x}_{1} + \dots + \beta_{k}\vect{x}_{k}\)` - `\(\vect{\Sigma}\)` es la matriz de varianza-covarianza entre las observaciones ] <br> -- visualmente: `$$\begin{bmatrix} y_{i} \\ \vdots \\ y_{n} \end{bmatrix}_{(n,1)} \sim \text{Normal}_{n}\Bigg( \vect{\mu} = \begin{bmatrix} \beta_{0} + \beta_{1}x_{1i} + \dots \beta_{k}x_{ki} \\ \vdots \\ \beta_{0} + \beta_{1}x_{1n} + \dots \beta_{k}x_{kn} \end{bmatrix}_{(n,1)} , \vect{\Sigma} = \begin{bmatrix} \sigma^{2} & 0 & \ldots & 0 \\ 0 & \sigma^{2} & \ldots & 0 \\ \vdots & \vdots & \sigma^{2} & \vdots \\ 0 & 0 & \ldots & \sigma^{2} \end{bmatrix}_{(n,n)}\Bigg)$$` --- ## Modelo de regresión lineal "Ensamblemos" el modelo via Monte Carlo Simulation. "Data Generating Process" (.bold[DGP]): -- ``` r set.seed(87742) # seed n <- 5000 # observaciones x <- sample(1:100,n,replace=TRUE) # 1 predictor o var independiente ``` ``` ## int [1:5000] 29 19 62 6 62 90 6 83 65 76 ... ``` ``` r # parámetros sigma <- 7 # sd b_0 <- 10 # intercepto b_1 <- 1.1 # coeficiente de x mu <- b_0 + b_1*x # valor predicho ``` ``` ## num [1:5000] 41.9 30.9 78.2 16.6 78.2 ... ``` ``` r # variable dependiente y <- rnorm(n,mu,sigma) # variable dependiente. Equivalente: y <- mu + rnorm(n,0,sigma) ``` ``` ## num [1:5000] 44.4 37.03 81.88 9.85 81.41 ... ``` --- ## Estimación modelo de regresión lineal: .pull-left[ .content-box-primary[ .bold[OLS] `$$\color{white}{\hat{\boldsymbol{\beta}}_{OLS} = \underset{\beta}{\arg\min\ } \sum_{i=1}^{n} (y_{i} - \vect{X}_{i}'\vect{\beta})^{2} \quad \text{ donde}}$$` ] ] .pull-right[ - `\(\vect{y}\)` es el vector `\(y_{i}, \dots, y_{n}\)` - `\(\vect{X}_{i}'\vect{\beta} = \beta_{0} + \beta_{1}x_{1i} + \dots + \beta_{k}x_{ki}\)` ] -- .pull-left[ .content-box-primary[ .bold[MLE] `$$\color{white}{\hat{\boldsymbol{\beta}}_{MLE} = \underset{\beta}{\arg\max\ } \prod_{i=1}^{n} \frac{1}{\sqrt{2\pi\sigma^{2}}} e^{- \frac{(y_{i} - \vect{X}_{i}'\vect{\beta})^{2}}{2\sigma^{2}}} \quad \text{ donde}}$$` ] ] .pull-right[ * `\(\frac{1}{\sqrt{2\pi\sigma^{2}}} e^{- \frac{(x - \mu)^{2}}{2\sigma^{2}}}\)` es la densidad de probabilidad de una variable aleatoria `\(X \sim \mathcal{N}(\mu,\sigma^2)\)`] <style type="text/css"> .pull-right ~ * { clear: unset; } .pull-right + * { clear: both; } </style> -- Ambos métodos producen mismos resultados en el caso de LM. --- ## Modelo de regresión lineal Ahora estimemos los parámetros de nuestro modelo via OLS ``` r our_data <- tibble(y=y, x=x) our_lm_ols <- lm(y ~ x, data=our_data) # "fit" el modelo usando función lm() print(summary(our_lm_ols)) # analicemos nuestros resultados ``` ``` ## ## Call: ## lm(formula = y ~ x, data = our_data) ## ## Residuals: ## Min 1Q Median 3Q Max ## -24.9776 -4.6438 0.0353 4.6418 25.1847 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 10.168799 0.193246 52.62 <2e-16 *** ## x 1.095101 0.003382 323.81 <2e-16 *** ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 6.943 on 4998 degrees of freedom ## Multiple R-squared: 0.9545, Adjusted R-squared: 0.9545 ## F-statistic: 1.049e+05 on 1 and 4998 DF, p-value: < 2.2e-16 ``` --- ## Modelo de regresión lineal Ahora estimemos los parámetros via MLE ``` r our_lm_mle <- glm(y ~ x, family="gaussian", data=our_data) # "fit" modelo usando función glm() print(summary(our_lm_mle)) # analicemos nuestros resultados ``` ``` ## ## Call: ## glm(formula = y ~ x, family = "gaussian", data = our_data) ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 10.168799 0.193246 52.62 <2e-16 *** ## x 1.095101 0.003382 323.81 <2e-16 *** ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## (Dispersion parameter for gaussian family taken to be 48.20756) ## ## Null deviance: 5295609 on 4999 degrees of freedom ## Residual deviance: 240941 on 4998 degrees of freedom ## AIC: 33571 ## ## Number of Fisher Scoring iterations: 2 ``` --- ## Modelo de regresión lineal .pull-left[ <!-- --> ] -- .pull-right[ Observamos que: - `\(\mathbb{E}(y_{i} \mid x = 50) = 64.9\)` - `\(\mathbb{E}(y_{i} \mid x = 60) = 75.9\)` - Estas "medias condicionales" no son determinísticas sino .bold[_probabilísticas_]. - Específicamente, sabemos que: - `\(y_{i} \mid x = 50 \sim \text{Normal}(\mu= 64.9, \sigma=7)\)` - `\(y_{i} \mid x = 60 \sim \text{Normal}(\mu= 75.9, \sigma=7)\)` ] --- ## Modelo de regresión lineal .pull-left[ <br> Así se ve: - `\(\mathbb{E}(y_{i} \mid x = 50) = 64.9\)` - `\(\mathbb{E}(y_{i} \mid x = 60) = 75.9\)` <br> donde: - `\(y_{i} \mid x = 50 \sim \text{Normal}(\mu= 64.9, \sigma=7)\)` - `\(y_{i} \mid x = 60 \sim \text{Normal}(\mu= 75.9, \sigma=7)\)` ] .pull-right[ <!-- --> ] --- ## Interpretación coeficientes en LM <br> `$$\text{Si } \quad \quad y_{i} = \overbrace{\beta_{0} + \beta_{1}x_{1i} + \dots \beta_{k}x_{ki}}^{\mathbb{E}(y_{i} \mid x_{1}, \dots, x_{k})} + \underbrace{e_i}_{\sim \text{Normal}(0,\sigma)}$$` --- ## Interpretación coeficientes en LM <br> `$$\text{Si } \quad \quad y_{i} = \overbrace{\beta_{0} + \beta_{1}x_{1i} + \dots \beta_{k}x_{ki}}^{\mathbb{E}(y_{i} \mid x_{1}, \dots, x_{k})} + \underbrace{e_{i}}_{\text{Normal}}(0,\sigma)$$` <br> Entonces decimos que el efecto de `\(x_{k}\)` sobre `\(y\)` es `\(\beta_{k}\)`. ¿Qué significa? .pull-left[ `$$\frac{\partial \mathbb{E}(y_{i} \mid x_{1}, \dots, x_{k})}{\partial x_{k}} = \beta_{k}$$` ] .pull-right[ "Un cambio en `\(\Delta\)` unidades de `\(x_{k}\)` se traduce en un cambio en `\(\Delta\)` `\(\beta_{k}\)` unidades en el valor esperado de `\(y_{i}\)`" ] --- ## Interpretación coeficientes en LM En nuestro ejemplo: .pull-left[ ``` r print(our_lm_ols) ``` ``` ## ## Call: ## lm(formula = y ~ x, data = our_data) ## ## Coefficients: ## (Intercept) x ## 10.169 1.095 ``` ] .pull-right[ Si `x=50`, entonces `y`= ``` r 10.2 + 1.1*50 ``` ``` ## [1] 65.2 ``` Si `x=51`, entonces `y`= ``` r 10.2 + 1.1*51 ``` ``` ## [1] 66.3 ``` Por tanto, `\(\beta\)`= ``` r ((10.2 + 1.1*51)-(10.2 + 1.1*50))/(51 - 50) ``` ``` ## [1] 1.1 ``` ] --- ## Interpretación coeficientes en LM Un ejemplo más complejo: podemos incluir interacciones y efectos no lineales ``` r set.seed("87742") # seed n <- 10000 # observaciones x <- sample(1:100,n,replace=TRUE) # variable independiente continua d <- sample(0:1,n,replace = TRUE) # dicotómica ``` ``` r # parámetros sigma <- 50 # sd b_0 <- 10 # intercepto b_1 <- 0.1 # coeficiente de variable x^2 b_2 <- 2 # coeficiente de variable dummy d b_3 <- 0.05 # coeficiente interacción x^2*d mu <- b_0 + b_1*I(x^2) + b_2*d + b_3*I(x^2)*d # valor predicho ``` ``` r # variable dependiente y <- mu + rnorm(n,0,sigma) ``` ``` ## 'AsIs' num [1:10000] 114.0630.... -6.40535.... 472.9015.... 36.26481.... 387.7212.... ... ``` --- ## Interpretación coeficientes en LM Estimamos los parámetros via OLS ``` r our_data2 <- tibble(y=y, x=x, d=d) our_lm_ols2 <- lm(y ~ I(x^2)*factor(d), data=our_data2) # "fit" el modelo usando función lm() print(summary(our_lm_ols2)) # analicemos nuestros resultados ``` ``` ## ## Call: ## lm(formula = y ~ I(x^2) * factor(d), data = our_data2) ## ## Residuals: ## Min 1Q Median 3Q Max ## -203.60 -32.74 0.05 33.05 181.90 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 9.3760348 1.0493901 8.935 <2e-16 *** ## I(x^2) 0.1002460 0.0002331 429.992 <2e-16 *** ## factor(d)1 0.1349249 1.4837465 0.091 0.928 ## I(x^2):factor(d)1 0.0499252 0.0003301 151.246 <2e-16 *** ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 49.45 on 9996 degrees of freedom ## Multiple R-squared: 0.9843, Adjusted R-squared: 0.9843 ## F-statistic: 2.089e+05 on 3 and 9996 DF, p-value: < 2.2e-16 ``` --- ## Interpretación coeficientes en LM .pull-left[ <!-- --> ] -- .pull-right[ `$$y_{i} = \beta_{0} + \beta_{1} x^{2}_{i} + \beta_{2}d_{i} + \beta_{3} x^{2}_{i} \cdot d_{i} + e_{i}$$` <br> Por tanto: `\begin{align} \mathbb{E}(y_{i} \mid x, d) = \begin{cases} \beta_{0} + \beta_{1} x^{2}_{i} &\quad \text{ si } d_{i}=0 \\ \\ (\beta_{0} + \beta_{2}) + (\beta_{1} + \beta_{3}) x^{2}_{i} &\quad \text{ si } d_{i}=1 \end{cases} \end{align}` <br> <br> Específicamente: `\begin{align} \frac{\partial \mathbb{E}(y_{i} \mid x, d) }{\partial x} = \begin{cases} 2 \beta_{1}x & \quad \text{ si } d_{i}=0 \\ \\ 2(\beta_{1} + \beta_{3})x & \quad \text{ si } d_{i}=1 \end{cases} \end{align}` ] --- class: inverse, center, middle ## El Modelo Lineal de Probabilidad (LPM) --- ## El Modelo Lineal de Probabilidad (LPM) .bold[LMP] es simplemente un modelo de regresión lineal aplicado a una variable dicotómica. Un LMP estándar tiene la siguiente forma: -- `$$y_{i} = \overbrace{\beta_{0} + \beta_{1}x_{1i} + \dots + \beta_{k}x_{ki}}^{\mathbb{E}(y_{i} \mid x_{1}, \dots, x_{k})} + e_{i} \quad \quad \text{ donde } y_{i} \in \{0,1\}$$` Dado que `\(y_{i} \in \{0,1\}\)`, * `\(\mathbb{E}(y_{i} \mid x_{1}, \dots, x_{k}) \equiv \mathbb{P}(y_{i} =1 \mid x_{1}, \dots, x_{k})\)` * Equivalentemente, `\(\mu_{i} \equiv p_{i}\)` <br> <br> -- Por tanto, en un LPM .content-box-primary[ `$$\color{white}{y_{i} \sim \text{Normal}(p_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma)}$$` ] --- ## LMP en la práctica Para ejemplificar el uso del LPM continuaremos trabajando con los datos de infidelidad. ``` ## # A tibble: 15 × 10 ## sex age ym child religious education rate nbaffairs everaffair ## <fct> <dbl> <dbl> <fct> <int> <dbl> <int> <dbl> <chr> ## 1 male 57 15 yes 4 20 4 0 Never ## 2 female 57 15 yes 4 16 4 0 Never ## 3 female 57 15 yes 2 18 2 0 Never ## 4 male 57 15 yes 4 9 2 0 Never ## 5 male 57 15 yes 4 20 5 0 Never ## 6 male 57 15 yes 2 20 4 0 Never ## 7 male 57 15 yes 4 9 4 0 Never ## 8 male 57 15 yes 4 17 5 0 Never ## 9 male 57 15 yes 5 18 2 0 Never ## 10 female 57 15 yes 3 18 2 0 Never ## 11 male 57 15 no 4 9 1 0 Never ## 12 female 57 15 no 4 20 5 0 Never ## 13 female 57 15 yes 1 18 4 2 At least once ## 14 male 57 15 yes 1 17 4 2 At least once ## 15 male 57 15 yes 5 20 5 7 At least once ## # ℹ 1 more variable: everaffair_d <dbl> ``` --- ## LMP en la práctica Ajustaremos el siguiente modelo: `\(\text{everaffair}_{i} = \beta_{0} + \beta_{1}*\text{rate}_{i}\)`, que modela la probabilidad de tener un affair como función de la evaluación de los entrevistados de su matrimonio, desde 1 (muy infeliz) a 5 (muy feliz). ``` r lpm_affairs_rate <- lm(everaffair_d ~ rate, data=affairsdata); summary(lpm_affairs_rate) ``` ``` ## ## Call: ## lm(formula = everaffair_d ~ rate, data = affairsdata) ## ## Residuals: ## Min 1Q Median 3Q Max ## -0.5417 -0.2428 -0.1431 -0.1431 0.8569 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 0.64140 0.06336 10.123 < 2e-16 *** ## rate -0.09965 0.01552 -6.422 2.74e-10 *** ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 0.4193 on 599 degrees of freedom ## Multiple R-squared: 0.06442, Adjusted R-squared: 0.06286 ## F-statistic: 41.25 on 1 and 599 DF, p-value: 2.736e-10 ``` --- ## LMP en la práctica .pull-left[ <!-- --> ] -- .pull-right[ .bold[Modelo] `\(\text{everaffair}_{i} = \beta_{0} + \beta_{1}*\text{rate}_{i}\)` Específicamente: `\(\frac{\partial \mathbb{P}(\text{affair}_{i}=1 \mid \text{ rate}) }{\partial \text{ rate}} = \beta_{1} = -0.1\)` .bold[Interpretación]: "Un cambio en `\(\Delta\)` unidades en la evaluación del matrimonio se traduce en un cambio en `\(\Delta\)` `\(\beta_{1}\)` unidades la probabilidad de haber tenido un affair" .bold[Ejemplo]: Diferencia en probabilidad de affair entre personas con matrimonio "muy infeliz" vs "muy feliz": `\((\beta_{0} + \beta_{1}) - (\beta_{0} + 5\beta_{1}) = -4\beta_{1} = 0.4\)` ] --- ## LMP en la práctica .content-box-primary[ `$$\color{white}{\text{LPM asume que: } \quad y_{i} \sim \text{Normal}(p_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma)}$$` ] <br> En este caso: `$$\text{everaffair}_{i} \sim \text{Normal}(\hat{p}_{i}= 0.64 - 0.1*\text{rate}_{i}, \hat{\sigma}=0.42)$$` donde `\(\hat{p}_{i} \in (0.14,0.54)\)` <br> -- Hasta aquí todo bien, pero ... --- ## Limitaciones del LMP .content-box-primary[ `$$\color{white}{\text{LPM asume que: } \quad y_{i} \sim \text{Normal}(p_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma)}$$` ] <br> .bold[1) Distribución y rango] - LPM asume que las observaciones `\(y_{i}, \dots, y_{n}\)` siguen una distribución normal, pero sabemos que no es así. `\(y_{i} \in \{0,1\}\)`. -- Derivado de lo anterior, - A pesar de que `\(y_{i} \in \{0,1\}\)`, las predicciones de un LPM no están restringidas a este rango. Teóricamente, `\(p_{i} \in \{-\infty,\infty+\}\)`. En la práctica `\(\hat{p}_{i}\)` puede salir de rango `\(\{0,1\}\)`, especialmente cuando la probabilidad marginal `\(\mathbb{P}(y=1)\)` es cercana a `\(0\)` o `\(1\)`. --- ## Limitaciones del LMP .bold[1) Distribución y rango] - El problema no es sólo que obtener probabilidades predichas menores que 0 o mayores que 1 no tiene sentido. - Cuando esto ocurre, los coeficientes estimados por el LMP son .bold[sesgados] e .bold[inconsistentes] - Más aún, en muestras grandes el problema es peor: converge hacia valores erróneos - Problema especialmente serio cuando el modelo produce una proporción alta de predicciones fuera de rango <br> .pull-left[  ] .pull-left[  ] --- .bold[Paréntesis: Sesgo (Bias) y Consistencia (Consistency) de un estimador] -- .pull-left[  ] -- .pull-right[  ] --- .bold[Paréntesis: Sesgo (Bias) y Consistencia (Consistency) de un estimador] -- .pull-left[  ] -- .pull-right[  ] --- ## Limitaciones del LMP .content-box-primary[ `$$\color{white}{\text{LPM asume que: } \quad y_{i} \sim \text{Normal}(p_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma)}$$` ] .bold[2) Observaciones con varianza heterogénea (o, errores heterocedásticos)] `\begin{align} \mathbb{Var}(y_{i}) &= \sum_{\text{valores } y_{i}} (y_{i} - \mathbb{E}(y_{i}) )^{2} \cdot \mathbb{P}(y_{i}) \\ &= \sum_{\text{valores } y_{i}} (y_{i} - p_{i})^{2} \cdot \mathbb{P}(y_{i}) \end{align}` --- ## Limitaciones del LMP .content-box-primary[ `$$\text{LPM asume que: } \quad y_{i} \sim \text{Normal}(p_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma)$$` ] <br> .bold[2) Observaciones con varianza heterogenea (o, errores heterocedásticos)] <br> `\begin{align} \mathbb{Var}(y_{i}) &= \sum_{\text{valores } y_{i}} (y_{i} - \mathbb{E}(y_{i}) )^{2} \cdot \mathbb{P}(y_{i}) \\ &= \sum_{\text{valores } y_{i}} (y_{i} - p_{i})^{2} \cdot \mathbb{P}(y_{i}) \\ \\ &= (1 - p_{i})^{2} \cdot \mathbb{P}(y_{i}=1) + (0 - p_{i})^{2} \cdot \mathbb{P}(y_{i}=0) \\ &= (1 - p_{i})^{2}p_{i} + (0 - p_{i})^{2} (1-p_{i}) \\ &= p_{i}(1-p_{i}) \end{align}` --- ## Limitaciones del LMP .bold[2) Observaciones con varianza heterogénea (o, errores heterocedásticos)] `\begin{align} \mathbb{Var}(y_{i}) &= p_{i}(1-p_{i}) \\ &= (\beta_{0} + \beta_{1}x_{1i} + \dots + \beta_{k}x_{ki})(1 - \beta_{0} + \beta_{1}x_{1i} + \dots + \beta_{k}x_{ki}) \end{align}` -- Por tanto, <br> .content-box-primary[ `$$\color{white}{\text{LPM asume que: } \quad y_{i} \sim \text{Normal}(p_{i}, \sigma) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma)}$$` ] <br> -- pero en realidad, <br> .content-box-secondary[ `$$\color{white}{y_{i} \sim \text{Normal}(p_{i}, \sigma_{i} = p_{i}(1-p_{i})) \quad \text{ o, equivalentemente: } \quad y_{i} = p_{i} + \text{Normal}(0, \sigma_{i} = p_{i}(1-p_{i}))}$$` ] --- ## Limitaciones del LMP en la práctica Para ejemplificar estas limitaciones del LPM estimemos un modelo ligeramente más complejo: `\(\text{everaffair}_{i} = \beta_{0} + \beta_{1}*\text{rate}_{i} + \beta_{2}*\text{rate}^{2}_{i} + \sum_{j}\vect{1} \{\text{rel}=j\}\Big( \beta_{0j} + \beta_{1j} \cdot \text{rate}_{i} + \beta_{2j} \cdot \text{rate}^{2}_{i}\Big)\)` ``` r lpm_affairs_raterel <- lm(everaffair_d ~ rate*factor(religious) + I(rate^2)*factor(religious), data=affairsdata) summary(lpm_affairs_raterel)$coefficients ``` --- ## Limitaciones del LMP en la práctica `\(\text{everaffair}_{i} = \beta_{0} + \beta_{1}*\text{rate}_{i} + \beta_{2}*\text{rate}^{2}_{i} + \sum_{j}\vect{1} \{\text{rel}=j\}\Big( \beta_{0j} + \beta_{1j} \cdot \text{rate}_{i} + \beta_{2j} \cdot \text{rate}^{2}_{i}\Big)\)` <br> ``` ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 1.93223443 0.60757213 3.1802552 0.001549173 ## rate -0.59564510 0.35259983 -1.6892949 0.091694858 ## factor(religious)2 -1.78379916 0.66768379 -2.6716227 0.007758429 ## factor(religious)3 -1.18924248 0.68392110 -1.7388592 0.082584703 ## factor(religious)4 -1.01501689 0.67535567 -1.5029368 0.133394036 ## factor(religious)5 -1.13934373 0.75671094 -1.5056525 0.132695217 ## I(rate^2) 0.05270655 0.04893715 1.0770254 0.281912084 ## rate:factor(religious)2 0.76126301 0.39243452 1.9398472 0.052877724 ## rate:factor(religious)3 0.58088887 0.40189195 1.4453857 0.148884129 ## rate:factor(religious)4 0.24746240 0.39320415 0.6293484 0.529366259 ## rate:factor(religious)5 0.28202792 0.44449596 0.6344893 0.526009189 ## factor(religious)2:I(rate^2) -0.08602173 0.05487567 -1.5675752 0.117520116 ## factor(religious)3:I(rate^2) -0.07467898 0.05622021 -1.3283299 0.184586222 ## factor(religious)4:I(rate^2) -0.01475551 0.05465733 -0.2699640 0.787283004 ## factor(religious)5:I(rate^2) -0.01503184 0.06208400 -0.2421210 0.808771116 ``` --- ## Limitaciones del LMP en la práctica .bold[Predicciones fuera de rango, sesgo e inconsistencia] .pull-left[ <!-- --> ] -- .pull-right[ <!-- --> ] --- ## Limitaciones del LMP en la práctica .bold[Errores heterocedásticos] .pull-left[ <!-- --> ] -- .pull-right[ <!-- --> ] --- ## Ventajas del LMP -- - Fácil de estimar: OLS -- - Fácil de interpretar: los coeficientes tienen una interpretación directa en términos de efectos parciales (marginales) sobre la _probabilidad_ de éxito en la variable dependiente. - Especialmente importante cuando trabajamos con modelos complejos: interacciones, efectos no-lineales, etc. -- - Permite una serie de extensiones propias de cualquier LM (.bold[mediación], variables instrumentales, efectos fijos) que con otros modelos para datos categóricos (ej, logit) no son posibles o son muy complejas. -- .pull-left[ Por lo mismo, hay .bold[mucho] interés en "rescatar" el LPM ] .pull-right[  ] --- ## Al rescate de LPM .bold[Problema: Observaciones con varianza heterogénea (heterocedasticidad)] `\(\quad \quad \Box\)` .bold[Solución: Errores Estándar "Robustos"] ``` r # Paquetes necesarios library(lmtest) library(sandwich) # Estimación del modelo lpm_affairs_raterel <- lm(everaffair_d ~ rate*factor(religious) + I(rate^2)*factor(religious), data=affairsdata) # Inferencia usando matrix de varianza-covarianza robusta (White method) coeftest(lpm_affairs_raterel, vcov = vcovHC(lpm_affairs_raterel, type="HC1")) ## type="HC3" es default R pero type="HC1" produce mismo resultados de Stata ``` --- ## Al rescate de LPM .bold[Problema: Observaciones con varianza heterogenea (heterocedásticidad)] `\(\quad \quad \Box\)` .bold[Solución: Errores Estándar "Robustos"] ``` ## ## t test of coefficients: ## ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 1.932234 0.548892 3.5202 0.0004646 *** ## rate -0.595645 0.347765 -1.7128 0.0872818 . ## factor(religious)2 -1.783799 0.623893 -2.8591 0.0043991 ** ## factor(religious)3 -1.189242 0.649859 -1.8300 0.0677576 . ## factor(religious)4 -1.015017 0.649529 -1.5627 0.1186639 ## factor(religious)5 -1.139344 0.755811 -1.5074 0.1322354 ## I(rate^2) 0.052707 0.050265 1.0486 0.2948060 ## rate:factor(religious)2 0.761263 0.392281 1.9406 0.0527854 . ## rate:factor(religious)3 0.580889 0.407477 1.4256 0.1545234 ## rate:factor(religious)4 0.247462 0.397200 0.6230 0.5335156 ## rate:factor(religious)5 0.282028 0.456356 0.6180 0.5368156 ## factor(religious)2:I(rate^2) -0.086022 0.056444 -1.5240 0.1280416 ## factor(religious)3:I(rate^2) -0.074679 0.058482 -1.2770 0.2021206 ## factor(religious)4:I(rate^2) -0.014756 0.056383 -0.2617 0.7936437 ## factor(religious)5:I(rate^2) -0.015032 0.064420 -0.2333 0.8155792 ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ``` --- ## Al rescate de LPM .bold[Problema: Predicciones fuera de rango, sesgo e inconsistencia] `\(\quad \quad \Box\)` .bold[Solución: No hay] -- `\(\quad \quad \Box\)` .bold[Paleativo: "trimming"] .pull-left[  ] .pull-left[  ] --- ## Al rescate de LPM .bold[Problema: Predicciones fuera de rango, sesgo e inconsistencia] `\(\quad \quad \Box\)` .bold[Paleativo: "trimming"] ``` r # Estimación del modelo lpm_affairs_raterel <- lm(everaffair_d ~ rate*factor(religious) + I(rate^2)*factor(religious), data=affairsdata) # Muestra recortada trimmed_sample <- affairsdata %>% mutate(fitted= lpm_affairs_raterel$fitted.values) %>% filter(between(fitted,0,1)) # Re-estimación del modelo en muestra trimmed lpm_affairs_raterel_trimmed <- lm(everaffair_d ~ rate*factor(religious) + I(rate^2)*factor(religious), data=trimmed_sample) summary(lpm_affairs_raterel_trimmed) ``` --- ## Al rescate de LPM .bold[Problema: Predicciones fuera de rango, sesgo e inconsistencia] `\(\quad \quad \Box\)` .bold[Paleativo: "trimming"] ``` ## ## Call: ## lm(formula = everaffair_d ~ rate * factor(religious) + I(rate^2) * ## factor(religious), data = trimmed_sample) ## ## Residuals: ## Min 1Q Median 3Q Max ## -0.7063 -0.2779 -0.1317 -0.1199 0.8801 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 3.06937 0.95990 3.198 0.00146 ** ## rate -1.18867 0.52390 -2.269 0.02364 * ## factor(religious)2 -2.92094 0.99895 -2.924 0.00359 ** ## factor(religious)3 -2.32638 1.00985 -2.304 0.02159 * ## factor(religious)4 -2.15216 1.00408 -2.143 0.03249 * ## factor(religious)5 -2.27648 1.06038 -2.147 0.03222 * ## I(rate^2) 0.12660 0.06874 1.842 0.06601 . ## rate:factor(religious)2 1.35429 0.55144 2.456 0.01434 * ## rate:factor(religious)3 1.17392 0.55819 2.103 0.03589 * ## rate:factor(religious)4 0.84049 0.55198 1.523 0.12838 ## rate:factor(religious)5 0.87506 0.58954 1.484 0.13827 ## factor(religious)2:I(rate^2) -0.15992 0.07308 -2.188 0.02904 * ## factor(religious)3:I(rate^2) -0.14858 0.07409 -2.005 0.04539 * ## factor(religious)4:I(rate^2) -0.08865 0.07291 -1.216 0.22453 ## factor(religious)5:I(rate^2) -0.08893 0.07862 -1.131 0.25848 ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 0.4096 on 585 degrees of freedom ## Multiple R-squared: 0.1239, Adjusted R-squared: 0.1029 ## F-statistic: 5.908 on 14 and 585 DF, p-value: 6.241e-11 ``` --- ## Al rescate de LPM .bold[Problema: Predicciones fuera de rango, sesgo e inconsistencia] `\(\quad \quad \Box\)` .bold[Paleativo: "trimming"] .pull-left[ <!-- --> ] .pull-right[ <!-- --> ] --- ## Esto no para ...[Wooldridge et al: "iterative trimming"] .pull-left[  ] .pull-right[  ] --- ## En resumen -- - LMP tiene muchas ventajas y muchos adeptos (economistas) debido a su parsimonia - LMP tiene también muchos problemas <br> -- ¿Son esas ventajas suficientes para contrapesar las desventajas? -- Depende del contexto, pero: <br>  --- class: inverse, center, middle ##Hasta la próxima clase. Gracias! <br> Mauricio Bucca <br> https://mebucca.github.io/ <br> github.com/mebucca